26 Aug The Fed’s liquidity train, what it means for gold, inflation and equities.

I had the good fortune to participate in a live webinar with the former head of Barings’ Research this week, Michael Howell, who runs CrossBorder Capital in London. A link to the presentation is available at the end.

Michael has specialised in the analysis of global liquidity flows for over three decades, and luckily for us, his views and work are still available.

In his third-quarter presentation “Liquidity, Capital flows and how they affect the Investment outlook” he draws out some interesting conclusions.

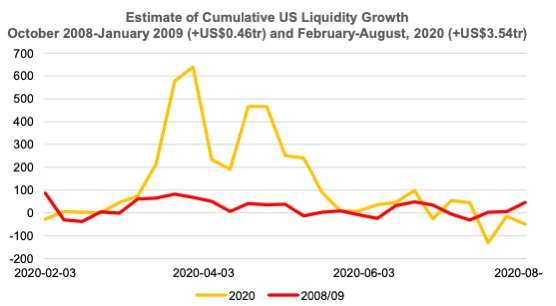

Global liquidity analysis is just one technique of analysing asset markets. My personal view is that liquidity continues to play a significant role, and the below chart from CrossBorder Capital places this quantitative easing (QE) programme into perspective.

As has been discussed by many experts, this recession is a government-induced slowdown in response to a health crisis. Unlike, the 2008/9 GFC, this is not a financial crisis, but a liquidity crisis. Hence, the record-breaking stimulus from the Federal Reserve.

According to CrossBorder Capital, the 2020 QE is five times that of 2008/9.

Source: CrossBorder Capital

This visual representation of 2020 QE programme (the yellow line) leaves no doubt about the enormity of this stimulus.

Anyone thinking that there may be a change of heart at the upcoming annual Jackson Hole Conference will most likely be disappointed. The head of the Federal Reserve, Jerome Powell, is hosting this conference virtually on Thursday, August 27.

According to Jonathan Pain, Author of the “The Pain Report,” Mr Powell will express what he termed the “third derivative”.

That is the Fed is “not even thinking about, thinking about, thinking about” raising interest rates. Source (CNBC: https://www.cnbc.com/2020/08/24/powell-set-to-deliver-profoundly-consequential-speech-changing-how-the-fed-views-inflation.html)

The term “lower for longer” may be reaching new bounds.

From my reading of the situation, Mr Powell will be talking about inflation and full employment targets. Most experts I have read, believe he will advocate for letting inflation run above the 2% target for longer to avoid what many economists call ‘Japanification’ or low growth, zero inflation and low-interest rates.

We could all argue about whether this form of stimulus is right or prudent, but the point is whether we like it or not, it will continue to happen. And our job as share investors is to manage our money within the limits of what we know.

I often hear experts criticising the Fed for what they call the Fed ‘put’ as coined to say the Fed has share markets’ backs. But in essence, it is what it is and “fighting the Fed” has proved pointless and costly for investors time and again.

So, what does Mike Howell make of all this liquidity?

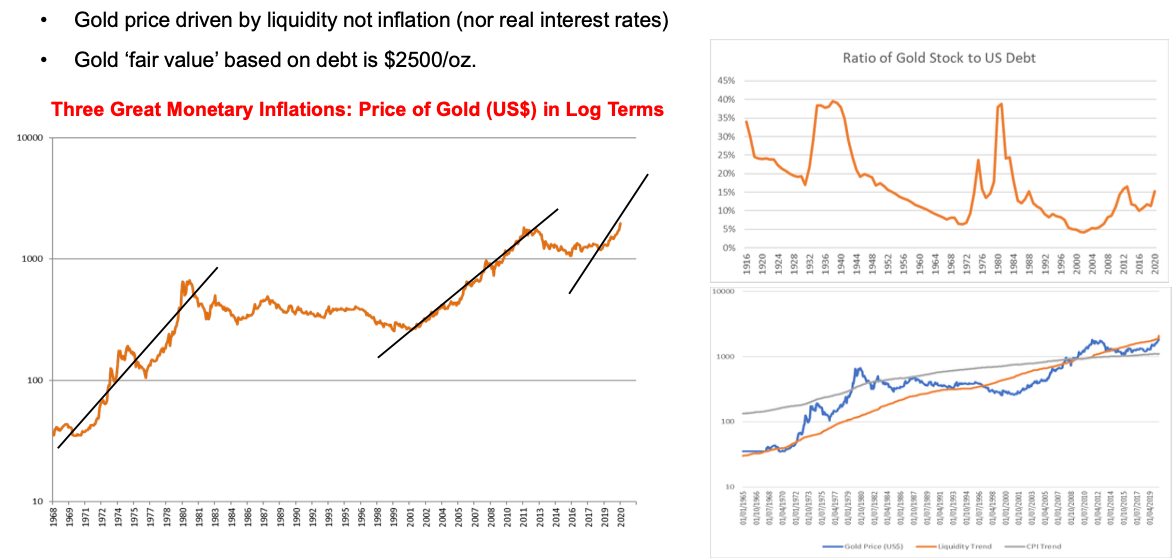

His report argues that the QE stimulus will continue to be supportive of gold. To explain his thinking, Mr Howell used the following three charts from the third-quarter presentation.

Source: CrossBorder Capital

The first chart shows the three waves of support for the gold price (on a logarithm scale) during periods of monetary expansion from the mid-1960s until the present day. The top-right chart shows the ratio of gold-stock to US debt. Mr Howell argues the production of gold is relatively restrained, so the price will rise instead to meet the long-term mean ratio to US debt of 25%. Under this proposition, the gold price could increase to US$2500 in the next two years.

The bottom right chart shows that the gold price is more reflective of monetary inflation (QE) than price inflation. In this chart, the gold price is the blue line, liquidity is orange, and the CPI (inflation) trend is grey. As you can see, the correlation is stronger between the gold price and monetary inflation.

Monetary inflation is the rise in asset prices. We have all witnessed the ‘V’ shaped recovery in the US share market, despite the worst economic recession since the Great Depression.

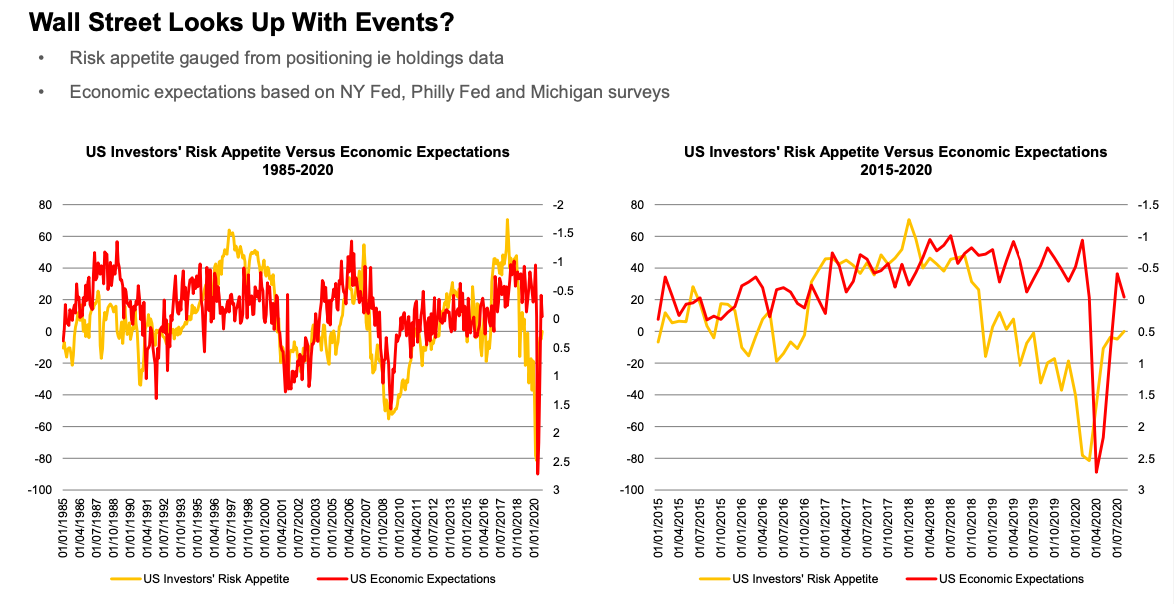

But before I move onto Mr Howell’s outlook for equities and inflation, I want to highlight just how ‘risk-averse’ the world became in March, April 2020. From personal experience, this sell-off was about as vicious and frightening as I have seen over my three decades of investing.

These charts from CrossBorder Capital show very clearly just how scared global investors were. Both charts plot similar information. The yellow line shows the risk appetite for US investors where zero is the mean. Anything above zero means the investors are happy to hold more risky assets like shares, and anything below means they are risk-averse and are holding more defensive assets, like cash and government bonds.

As the charts show, the risk aversion was the highest seen as far back as 1985. Mr Howell mentioned that one of their US clients were aware Fidelity had up to 20% of their client base who had entirely sold out of equities in this period.

If you thought the March 2020 sell-off was a historical event, then you would be correct.

Source: CrossBorder Capital

Since March, the US share market has experienced a ‘V’ shaped recovery, led mostly by technology shares and winners of the liquidity stimulus. But you all know this.

So, where to from here?

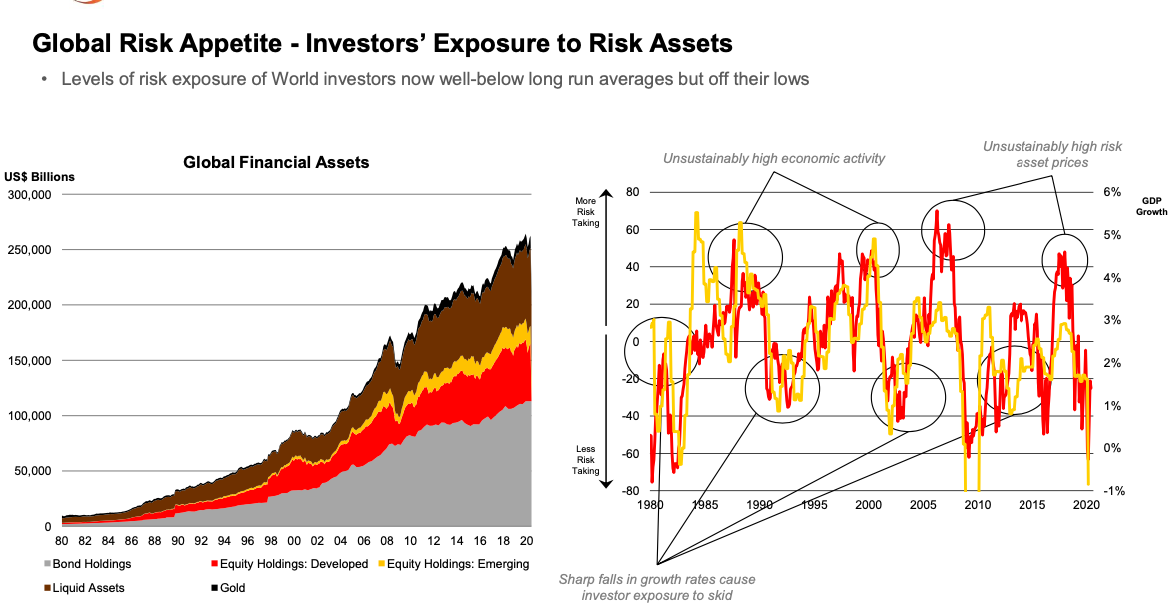

The first chart, below, shows the spread of global financial assets (in USD) across different asset classes. As you can see the red portion, representing the equity (shares) holding for the developed markets (such as the USA, Australia, UK, Europe and Japan) have not expanded even with all the QE stimulus.

The chart on the right shows that even though investors are taking on more risk (the yellow line), on balance, the levels remain well below previous bubbles such as the DOTCOM boom in 2000 and the property bubble of 2007.

Mr Howell discussed how equity markets are driven more by emotion than bond markets. Often the level of bullishness (or risk disposition) will pre-empt economic activity.

Whilst some experts worry about valuations and the concentration of the performance in the technology sector, these indicators would suggest the QE programmes remain bullish for shares.

Source: CrossBorder Capital

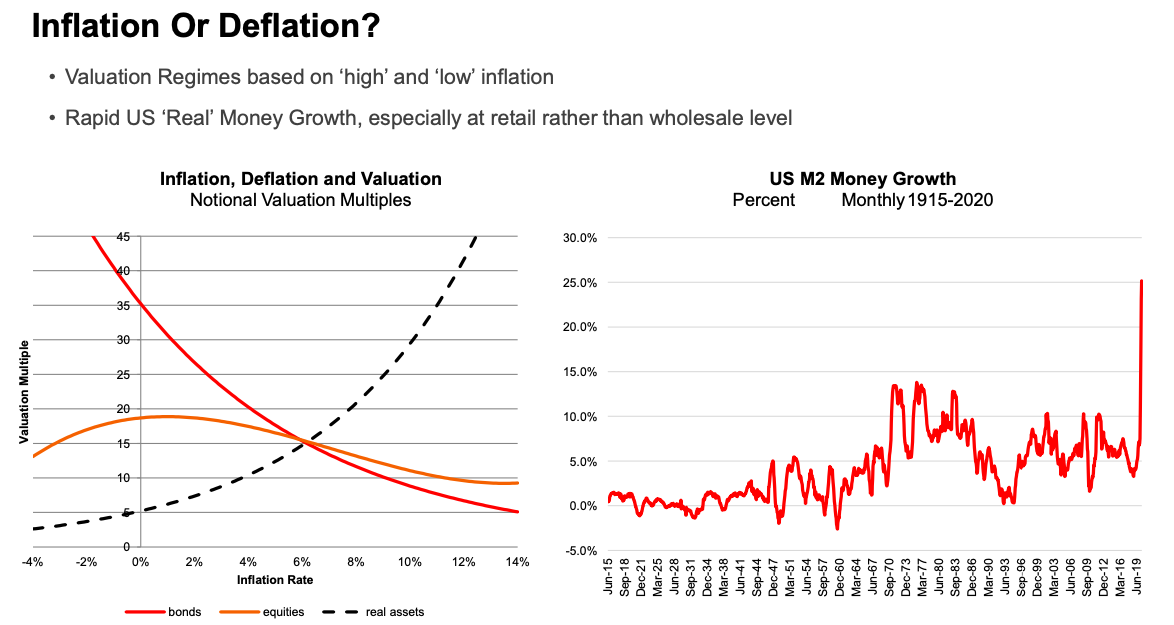

Before I finish up, there is one constant concern for share investors – price inflation.

Mr Howell’s charts tell a picture again. The right-hand shows the extent of the pickup in US monetary growth, M2. In economic jargon, historically, the increase in M2 leads to higher price inflation.

You may also be one of the many share investors who are worried about inflation, and a hedge is to buy gold. Gold ETFs are a reasonable way to gain exposure if you don’t want to buy gold shares.

However, contrary to what you may hear from other experts, there is evidence that some inflation offers a sweet spot for shares.

The left table shows the three main asset classes, shares (orange line), bonds (corporate and government – red line) and hard assets like property (the dotted line). Inflation is along the horizontal line, and as it increases, hard asset prices rise, bond and shares fall.

At 1-2%, there is a sweet spot for shares. Generally, if the companies are price makers, not takers then, stocks will outperform bonds as inflation rises.

Although inflation failed to pick up to the desired level post the GFC, despite all the stimulus, the record QE is undeniably causing some share investors to worry.

Whilst, I cannot replicate the detail or level of knowledge and expertise of Mr Howell, I wanted this post to introduce investors to concepts of liquidity analysis and what it means for assets. More specifically shares, bonds and gold.

If you would like more information, the presentation is available on YouTube, CrossBorder “Liquidity, Capital flows and how they affect the Investment outlook and conclusions”.

This was written on Wednesday, August 27 and represented only the views of Danielle Ecuyer, Author of Shareplicity. The Author holds or has held some of the shares discussed in her SMSF. Please read the disclaimer.

DISCLAIMER – Shareplicity offers information that is only general in nature. It does not take into account your personal financial situation, needs or objectives. Nor does it take into account the financial needs of any specific person. You should consider your own personal financial situation and needs or seek financial advice before making any decisions based on this information.